Why use Deputy? Benefits and a client profile

Deputy is a powerful piece of software renowned for making businesses smart, quick and simple. With more than 290,000 happy clients that continue to advocate for the software, Deputy is transforming the landscape of Australian business operations.

Overview

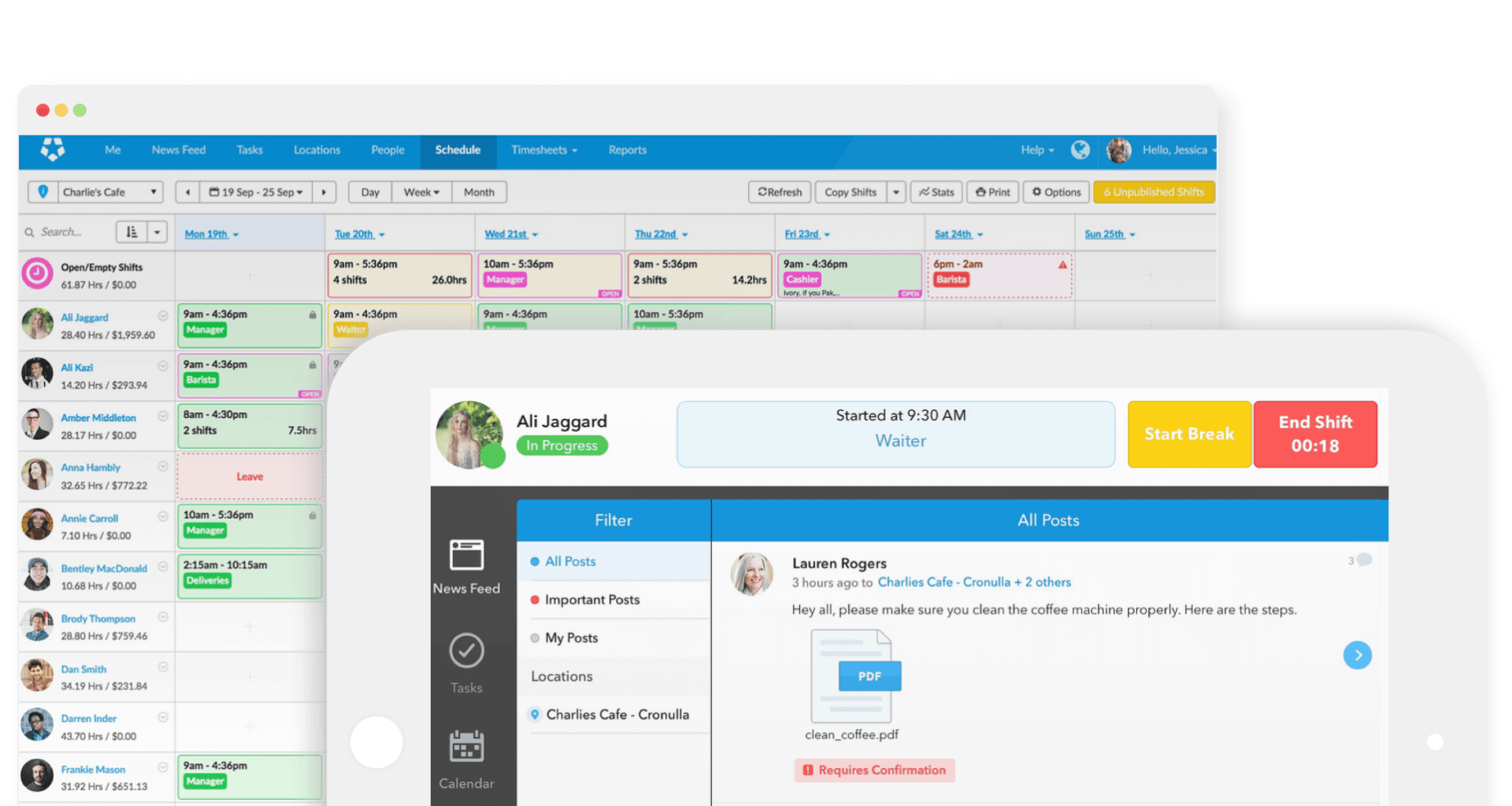

The purpose of Deputy is to streamline the way your business functions. As a comprehensive all-in-one platform, Deputy provides all of the core features you need to continue running your business on a day-to-day level - as well as planning ahead.

Key features of Deputy include employee onboarding, time tracking, rostering and more. Also available on mobile, Deputy is perfect for maintaining business operations whilst on the go.

Benefits of using Deputy

There are many benefits that come with using Deputy. We've outlined some of the main reasons why you should consider integrating Deputy into your business.

Versatility

Deputy was developed with the intention of providing everything your business needs at an administrative level. Because of this, it's the ideal tool for businesses that require versatility in their software. From tracking payroll to communicating with team members, Deputy is equipped with all of the features you need.

Accessibility

Another benefit of Deputy is just how simple and straightforward it is to use. With tours available, even the most technophobic of business owners can begin using Deputy right away. If you're familiar with business management software already, Deputy will feel like home. Our interface is clean, making navigation around the software a breeze.

Mobility

As mentioned previously, Deputy is available as an app. This means that you can keep track of much of your business's operations whilst out of office. This boosts your feeling of security that the business is only a few clicks away if urgent changes need to be made. New users can also be added on an as and when needed basis, perfect for onboarding new employees.

Flexibility

Deputy is able to be integrated with many existing HR software, as well as your current payroll and POS systems. This makes it an incredibly flexible piece of software that you can introduce to operations easily. Deputy is also flexible in that it's able to be used by various industries, including hospitality, retail, healthcare, call centres and more.

Security

Ultimately, Deputy was developed with the growth and continual health of your business in mind. This means that the software boasts fantastic data security, including meeting key industry standards such as being PCI compliant. Annual audits and frequent security assessments are also completed to ensure that our infrastructure remains safe.

How our client "Kinfolk" uses Deputy and Xero

How does Deputy increase staff efficiency?

Deputy's real-time performance review features allow employers to give feedback after every shift and increase employee morale by celebrating top performers and providing support to those who need more assistance. A performance record can also be maintained which can be used to identify trends in job performance and assist in the generation of reports. Employee satisfaction can also be tracked through the rating given by the staff member after completing their shift.

How does Deputy help with staff costing and budgeting?

Deputy shows staff costs while scheduling shifts based on the pay rates assigned to them. This helps in staff allocation based on the budgets for the week or month. Also, the "start shift" and "end shift" options along with 'start break' and 'end break' given to employees during their shifts allow for accurate wage payments based on the actual hours worked. The reports function in deputy helps in monitoring the sales v/s work schedule of employees for a particular week and gives a snapshot of the total costs incurred v/s revenue generated for the week. It also syncs revenue information from the POS system which helps with staff allocation.

How Deputy's award rate interpretation removes the guesswork?

Deputy has multiple award rates based on occupation and level of skills (for example, Chefs come under restaurant industry award (RIA) for level 1-2, and 3 and above). The system automatically calculates rates for weekends, public holidays, night shifts, etc which saves a lot of time.

How do Xero and Deputy sync and create efficiencies?

Deputy allows timesheets to be exported to Xero, and syncs the base pay rates and employee details from Xero. This simplifies the payroll process as updates can be done in one platform and can be synced to another in a short span of time.

Begin using Deputy today

Whether you're a small start-up firm, an SME or a global business chain, Deputy is the perfect software solution for your business needs. To get started, download today for a free trial. You can also contact a member of our friendly team to learn more about the services Deputy offers and how it can revolutionise the way your business works.

newsletter here!

Share This Post